An ESG materiality assessment helps businesses identify which environmental, social, and governance (ESG) issues matter most to their operations and stakeholders. Instead of addressing every possible issue, this process prioritizes topics that significantly impact financial performance and societal influence. The result? A focused approach to managing risks, meeting regulatory requirements, and aligning sustainability efforts with business goals.

Key Takeaways:

- Materiality Matrix: A tool that evaluates issues based on their importance to stakeholders and their impact on business success.

-

Types of Materiality:

- Financial: Focuses on ESG factors' effects on revenue, costs, and value.

- Impact: Examines how a company affects society and the environment.

- Double: Combines both perspectives, now required under EU regulations like CSRD.

- Why It Matters: Companies with strong ESG practices report higher revenue growth (16%) and profitability (52%) compared to peers.

- Who Needs It: Businesses aiming to comply with global frameworks like ISSB, GRI, SASB, and CSRD.

Process Overview:

- Define Scope: Decide which parts of the business and value chain to include.

- Engage Stakeholders: Gather insights from employees, investors, regulators, and more.

- Prioritize Topics: Use data to rank issues by financial and societal impact.

- Validate Findings: Secure leadership approval and align with disclosure frameworks.

- Integrate Results: Embed findings into risk management and strategy.

Why Now? With evolving regulations like the EU’s CSRD and growing investor expectations, materiality assessments are no longer optional - they’re essential for staying competitive and compliant.

Regulatory and Strategic Context

How Global ESG Standards Address Materiality

When it comes to materiality, four major frameworks - ISSB, GRI, SASB, and CSRD/ESRS - each provide unique perspectives, shaping how organizations assess and report on environmental, social, and governance (ESG) factors. Understanding these differences is crucial, especially as regulations continue to evolve:

| Framework | Materiality Lens | Primary Audience |

|---|---|---|

| ISSB (IFRS S1/S2) | Financial materiality | Investors, lenders, creditors |

| GRI Standards | Impact materiality | Employees, communities, NGOs |

| CSRD / ESRS | Double materiality (financial + impact) | Investors and broad stakeholders |

| SASB | Financial materiality (industry-specific) | Investors |

Each framework approaches materiality from a distinct angle. For example, ISSB focuses on financial materiality, defining material information as anything that could influence decisions made by users of general-purpose financial reports. On the other hand, GRI emphasizes how a company’s operations impact the world, regardless of financial implications. SASB, while aligned with ISSB, offers industry-specific guidance, pinpointing the ESG topics most likely to carry financial weight for a particular sector.

The CSRD/ESRS framework combines both financial and impact materiality, reflecting the broader expectations of investors and stakeholders. Regulatory shifts, like the Omnibus I Directive (effective February 2026), have further refined reporting requirements. Companies with over 1,000 employees and €450 million (~$490 million) in annual net turnover are now required to comply, narrowing the scope of affected entities from about 45,000 to 10,000. Additionally, both CSRD and ISSB mandate value chain coverage, extending reporting to include upstream suppliers and downstream customers. These changes not only redefine compliance but also influence strategic decision-making.

Strategic Value of Materiality Assessments

Materiality assessments go beyond regulatory compliance - they’re a tool for sharpening strategy. By identifying what truly matters, these assessments help organizations allocate resources effectively and manage risks more proactively. In essence, they guide leadership on where to focus sustainability efforts, which risks to prioritize, and how to refine capital allocation.

"Materiality determines disclosure scope; strategy determines resource allocation." - ESGsource

The outcomes of a materiality assessment should integrate directly into the enterprise risk management process, ensuring sustainability issues are reflected in the Chief Risk Officer’s risk register. Cross-functional collaboration is essential here. Teams from Finance, Legal, HR, Operations, and Risk must work together to ensure the assessment captures the full scope of the business. Increasingly, boards are expected to validate the final list of material topics, signaling strong governance and meeting CSRD requirements.

Most large organizations identify 8–15 material topics as their focus. If the list grows beyond 20, it’s often a sign that thresholds for materiality weren’t applied rigorously enough. Precision is critical because:

"A weak materiality process creates weak everything downstream." - ESGsource

sbb-itb-97f6a47

ESG Materiality Assessment and Sustainability Reporting 2025 Programme

How to Conduct an ESG Materiality Assessment

ESG Materiality Assessment Process: 5 Steps to Strategic Sustainability

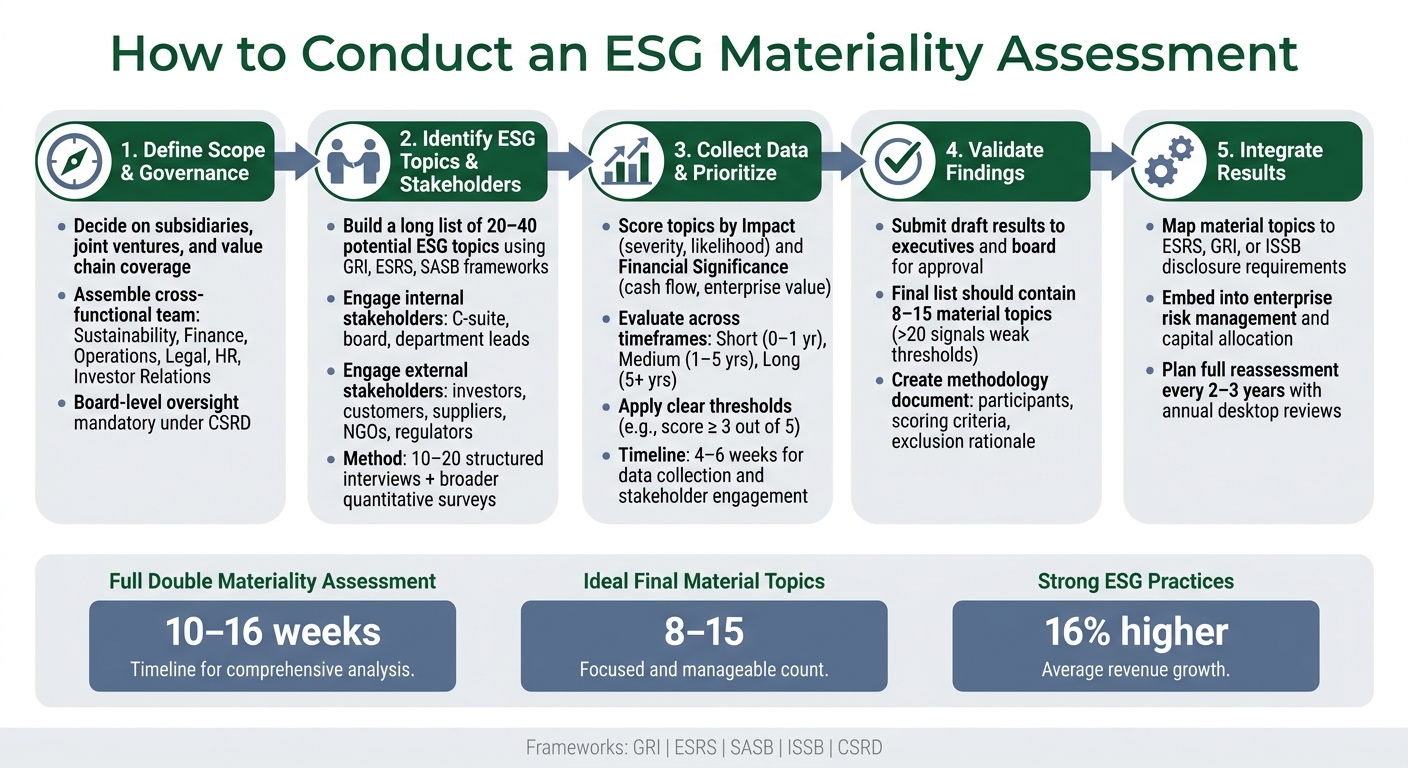

Planning and Governance

Start by clearly defining the scope of your assessment and assigning ownership from the beginning. This means deciding whether to include subsidiaries and joint ventures, as well as determining how far into your value chain you'll go - covering both upstream suppliers and downstream customers.

Equally important is setting up a strong governance structure. Assemble a cross-functional team with representatives from Sustainability, Finance, Operations, Legal, HR, and Investor Relations. Each department brings its own perspective, and failing to include diverse voices could lead to blind spots. Under CSRD, board-level oversight is not just recommended - it’s mandatory.

Identifying ESG Topics and Stakeholders

Begin by creating a "long list" of 20–40 potential ESG topics. Use frameworks like ESRS, GRI, and SASB, along with peer reports and regulatory reviews, to guide this process. This groundwork ensures stakeholder discussions are based on solid, relevant topics rather than open-ended brainstorming.

Next, engage stakeholders. Include both internal participants (C-suite, board members, and department leads) and external voices (investors, customers, suppliers, NGOs, and regulators). To cover both financial and impact materiality effectively, use a phased approach. Start with 10–20 structured interviews to gather qualitative insights, followed by broader quantitative surveys to generate scoring data.

Once you’ve gathered stakeholder input, refine your topic list and begin quantifying and ranking each one.

Data Collection and Prioritization

Evaluate ESG topics based on their impact (severity and likelihood on people and the environment) and financial significance (effects on cash flow and enterprise value) across short (0–1 year), medium (1–5 years), and long-term (5+ years) timeframes.

To keep the process objective and repeatable, establish clear thresholds before finalizing results - such as requiring a score of 3 or higher out of 5. For human rights topics, prioritize severity over likelihood. Typically, data collection and stakeholder engagement take 4–6 weeks, while a full double materiality assessment can be completed within 10–16 weeks.

"A materiality assessment that includes everything is as useless as one that includes nothing. The goal is focus." - Council Fire Resources

With scores in hand, the next step is to validate the findings with leadership.

Validation and Integration

Submit draft results to executives and the board for approval to ensure alignment with strategic priorities and gain leadership buy-in. If your final list includes more than 20 topics, revisit your thresholds - this could indicate they weren’t applied rigorously enough.

After validation, map each material topic to the relevant disclosure requirements under ESRS, GRI, or ISSB. This mapping forms the foundation of your sustainability report and data collection plan. Also, create a methodology document that outlines who participated, the scoring criteria, and the reasoning behind excluding certain topics. Auditors will closely examine these omissions. Plan for a full reassessment every 2–3 years, with annual desktop reviews to ensure your conclusions remain valid.

| Integration Phase | Key Action | Purpose |

|---|---|---|

| Validation | Board/executive approval | Aligns results with strategy and secures leadership commitment |

| Reporting | Map to ESRS/GRI/ISSB | Provides a framework for data collection and disclosure |

| Operations | Capital allocation & target setting | Transforms ESG from a reporting task into a driver of value creation |

| Assurance | Methodology documentation | Ensures transparency and supports third-party audits |

Double Materiality and Advanced Topics

How to Apply Double Materiality in Practice

Double materiality looks at ESG issues from two angles: impact materiality (inside-out) and financial materiality (outside-in).

"A sustainability matter is material from a financial perspective if it triggers material financial effects on the undertaking." - ESRS 1 General Requirements

Under ESRS guidelines, these two perspectives are treated independently - meaning a topic is deemed material if it meets either threshold. Impact materiality focuses on factors like scale, scope, and how difficult it is to reverse harm, while financial materiality considers the likelihood and size of potential financial consequences.

For companies operating across multiple regions, geography plays a critical role. Material impacts often vary by location. For example, a facility in Texas may face water stress, while one in the Pacific Northwest does not. In such cases, disaggregated reporting by geography helps capture these differences. A practical example is Dekker Chemie B.V., which initially identified 52 potential impacts and classified 28 as material using a severity scale of 1–5, with a cutoff at 3.0. After acquiring a Polish adhesives firm, they updated their assessment in just four days.

Scenario Planning and Risk Integration

Once double materiality is assessed, companies need to embed these insights into their risk management strategies. Identifying material topics is just the beginning; the real value comes from integrating these findings into scenario planning and overall risk frameworks.

A robust materiality assessment should connect directly to an enterprise's risk management and long-term strategy. This ensures companies remain prepared for how material issues might evolve in the short term (0–1 year), medium term (1–5 years), and long term (5+ years).

One important consideration is secondary risk identification - evaluating whether addressing one material issue creates new risks. For instance, an ambitious decarbonization plan might successfully lower Scope 1 emissions but lead to significant workforce impacts, such as layoffs or site closures. If a company determines that climate change is not currently material, ESRS mandates a detailed explanation alongside a forward-looking analysis of conditions that could change that conclusion.

"Double materiality operates as an overarching filter: only material information is required to be disclosed. The fair presentation principle governs the sustainability statement as a whole." - EFRAG, Simplified ESRS 1

On the regulatory front, the 2026 Omnibus I Directive narrowed mandatory CSRD reporting to companies with over 1,000 employees and net turnover exceeding €450 million (~$484 million). This adjustment excluded roughly 80% of the originally targeted companies. Despite this, EFRAG's 2025 implementation review revealed that over 40% of assessed companies still lacked a solid double materiality framework. This highlights that even with regulatory relief, prioritizing a thorough assessment remains a strategic necessity.

Tools and Resources for ESG Materiality

Using Technology and Data in Materiality Assessments

Modern platforms like Sprih simplify materiality assessments by combining workflows for stakeholder engagement, topic prioritization, and automatic framework alignment. This streamlined approach not only shortens the process but also helps teams stay organized when managing 30 to 50 sustainability topics across various stakeholder groups.

"Your materiality assessment is the foundation of credible sustainability reporting." - Sprih

When evaluating tools, two features stand out. First, audit trail generation is essential. These tools track who was engaged, when, and how - critical information since assurance providers often scrutinize the process as much as the outcomes. Second, weighting and calibration controls let teams assign appropriate influence to different inputs, such as giving more weight to a workshop with multiple perspectives than to a single survey response. This improves the accuracy of scoring. While Excel can work for simpler setups, it often struggles to keep up with increasing complexity.

"Subjectivity is inherent and acknowledged in the ESRS framework. This is why the process and documentation are as important as the numbers." - Kathrin Jansen, Double Materiality Expert, Dazzle

When to Bring in Outside Expertise

While technology makes data management easier, some situations call for outside help. External expertise is especially valuable when internal teams lack a solid scoring methodology. In fact, two-thirds of early Double Materiality Assessments reviewed by experts lacked defensible scoring methods or were too generalized to align with specific disclosure requirements. Fixing these issues later can be costly.

Consultants bring credibility and specialized skills, particularly for facilitating stakeholder discussions and conducting in-depth IRO (Impact, Risk, Opportunity) analyses. These experts can refine broad topics into actionable insights, typically completing the process in 4–8 weeks - far more thorough than a rushed 2-week assessment. For businesses seeking trusted ESG consultants, the Top Consulting Firms Directory is a useful resource for finding professionals in risk management, strategy, and financial advisory.

Common Challenges and How to Address Them

Even with advanced tools and expert help, organizations often face significant hurdles. One major challenge is engaging stakeholders at scale. Coordinating input from 50–100 external stakeholders and over 200 employees requires careful planning. Digital survey tools with prebuilt templates can assist, but assigning a dedicated team to manage outreach, follow-ups, and data consolidation is critical.

Another common issue is incomplete documentation. To avoid gaps, ensure that all scoring decisions are thoroughly recorded for auditor review. Establishing strong documentation habits from the start is far more effective than trying to piece things together later. Additionally, running calibration workshops - where team members independently score the same IRO and then compare results - can reduce inconsistencies and create a clear, defensible record.

Conclusion and Key Takeaways

Recap of the Materiality Assessment Process

Conducting an ESG materiality assessment involves several key steps. It starts with defining the scope and governance framework, followed by generating a list of 20–40 potential topics using established frameworks like GRI, ESRS, or SASB. Engaging a diverse range of stakeholders helps refine this list down to the 8–15 issues that are most critical. The process concludes with board validation and aligning findings with disclosure requirements to inform strategic decisions. A comprehensive double materiality assessment typically takes 10–16 weeks. While this timeline may seem extensive, the rigorous approach ensures that the results are both credible and defensible. Proper documentation is crucial for maintaining transparency, whether for internal purposes or external audits. This methodical process sets the stage for sustainable growth and effective risk management.

Final Thoughts on ESG Materiality

Following this structured approach offers clear strategic advantages. Research highlights that embedding sustainability practices can lead to measurable business benefits, including a 16% increase in revenue growth, a 52% boost in profitability, and improvements in EBITDA margins and exit multiples.

"Done correctly, sustainability drives resilience, reduces risk, and enhances long-term value." - Wellington Management

However, the real risk lies in viewing materiality as a one-and-done activity. With regulations and stakeholder expectations constantly evolving, materiality must be treated as a dynamic process. Regular reassessments every 2–3 years, along with annual desktop reviews, are essential to ensure that strategies remain aligned with the most pressing issues of the moment. By treating materiality as an ongoing effort, organizations can stay ahead of changes and maintain a focus on what truly matters.

FAQs

How do I decide which ESG topics are truly material for my company?

To pinpoint the most critical ESG (Environmental, Social, and Governance) topics for your business, a formal materiality assessment is essential. This process ensures your ESG strategy aligns with both your company’s operations and the expectations of stakeholders.

Start by mapping your value chain - this means examining every step of your business operations, from sourcing materials to delivering products or services. Once you’ve done that, compile a list of 20 to 50 potential ESG topics. You can use established frameworks like ESRS (European Sustainability Reporting Standards), GRI (Global Reporting Initiative), or SASB (Sustainability Accounting Standards Board) to guide you in identifying relevant issues.

Next, assess these topics using two key lenses:

- Impact Materiality: How does your company influence the environment, society, and governance? This looks at the broader effects your business has on the world.

- Financial Materiality: How do these ESG topics affect your company’s enterprise value? This focuses on risks and opportunities that could impact your financial performance.

To refine and prioritize these topics, engage with your stakeholders. This could include employees, investors, customers, suppliers, and community representatives. Their input will help you determine which issues are the most significant and should be addressed in your strategy and disclosures.

By following this structured approach, you’ll have a clear roadmap to identify and act on the ESG topics that matter most to your business and its stakeholders.

Do I need double materiality if my business is based in the United States?

If your U.S.-based business has substantial operations or commercial connections within the European Union, you’re likely required to comply with the Corporate Sustainability Reporting Directive (CSRD). This includes conducting a double materiality assessment. Essentially, this means you’ll need to report on sustainability topics that are material from either an impact perspective, a financial perspective, or both.

Even if your business isn’t obligated to follow the CSRD, adopting double materiality is widely regarded as a strong approach for enhancing accountability and managing risks effectively.

What evidence and documentation will auditors expect from a materiality assessment?

Auditors need well-organized documentation to confirm the objectivity and depth of your materiality assessment. This means laying out your methodology in detail - explain the criteria and thresholds you used to pinpoint critical impacts, risks, and opportunities.

Make sure to include records of stakeholder engagement. This should cover who was involved, when the engagement took place, and how their feedback influenced your assessment. Additionally, provide evidence that clearly connects the topics you identified to your overall business strategy.

Having a transparent, audit-ready documentation trail isn't just helpful - it’s essential for meeting compliance requirements under frameworks like CSRD.